Autumn Statement 2023 and seven key developments and their Impact on businesses. 1. National Insurance Adjustments: A Relief for Employees and the Self-Employed The government has announced a reduction in National Insurance contributions for employees by 2%, affecting approximately 27 million people, effective from January 6, 2024. Additionally, the abolition of class 2 National Insurance will benefit self-employed individuals, saving them around £192 annually. Moreover, class 4 National Insurance will be reduced from 9% to 8% for earnings between £12,570 and £50,270.

2. Corporate Taxation: Maintaining the Status Quo, The increase in Corporation Tax, from 19% to 25% for profits exceeding £250,000, will continue. To stimulate business investments in technology, equipment, and plant & machinery, full capital allowances will be fully deductible. 3. Inflation Trends: A Positive Shift In a significant economic turnaround, the UK saw a drop in inflation to 4.6% this October, a notable decrease from the staggering 11.1% at the beginning of the year. While this reduction signals a positive shift, the government's forecast indicates a gradual path to the target inflation rate of 2%, anticipated to be achieved by 2025. 4. Economic Growth and Recession Concerns the Office for Budget Responsibility (OBR) had earlier projected a recession in the UK. Contrasting this, the Chancellor recently expressed a more optimistic outlook, expecting the UK economy to grow by 0.6% this year. Furthermore, government debt has seen a reduction from initial forecasts, alongside a decrease in borrowing costs. From 2024, the UK economy is expected to witness a growth phase, offering a ray of hope for businesses and investors. 5. Employment Incentives The employment allowance will continue at the elevated level of £5,000, providing further support to businesses. 6. Capital Gains Tax: A Notable Change Beginning April 2024, the 'annual exemption' amount in Capital Gains Tax will be halved from £6,000 to £3,000, a change that businesses and investors need to prepare for. 7. Additional Economic Measures

These developments reflect a blend of challenges and opportunities for UK businesses. While some measures, like the reduction in National Insurance and the retention of the employment allowance, offer immediate relief, others like the changes in Capital Gains Tax and Corporation Tax require strategic planning. The overall economic forecast, however, paints a cautiously optimistic picture for the coming years.  Grants and loans are both mechanisms to secure funding, but they differ significantly in terms of their structure, purpose, and obligations.

Here's a comparison: 1. Definition:

To learn more or if you are interested in a business loan or business grant, please contact RBSS Consulting Ltd on 033 33 55 1696 or email us on info@rbssconsulting.com. 5 strategies small businesses can adopt to thrive in an environment of rising interest rates11/8/2023

To help to get inflation back down; on 3 August 2023, the bank of England raised our interest rate (Bank Rate) by 0.25 percentage points to 5.25%. This is its highest level since February 2008. This has a huge impact on businesses, most especially small businesses which are often dependent on external finance for growth and investment. The increased cost of borrowing therefore makes it more difficult for them to get help to raise finance they need to thrive. Hence, such businesses need to be more proactive and strategic in their financial management to keep afloat. Here are five specific steps and strategies they can implement:

By implementing the above business improvement strategies and maintaining a proactive approach to financial management, small businesses can rise above the challenges of the rising interest rates and position themselves for long-term success and growth. If you need help in any of the above pointers or others regarding the rise in interest rates, give us a call today on 0333 355 1696 or send us a message at info@rbssconsulting.com.

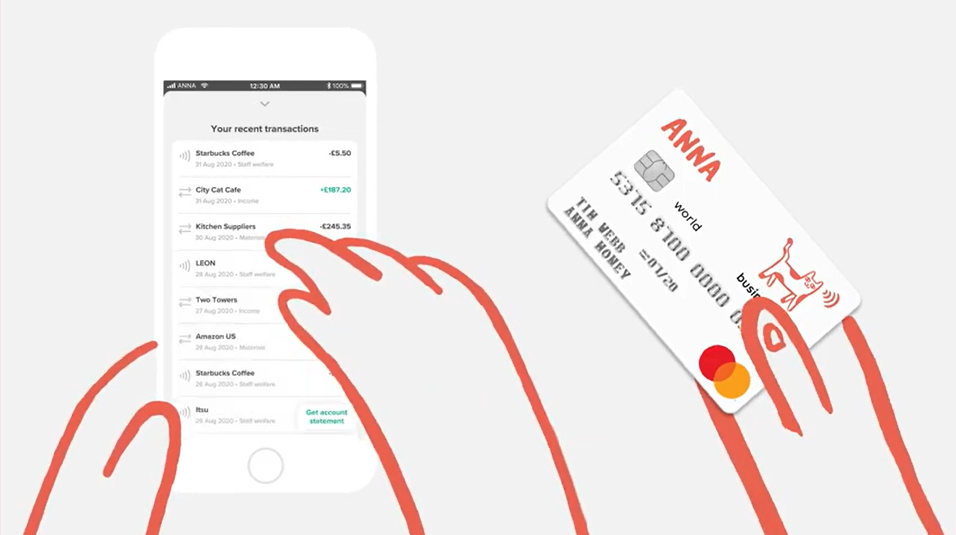

RBSS Consulting Ltd have teamed up with ANNA Money.

You shouldn’t have to wait hours to speak to your bank. That’s why we have teamed up with ANNA Money who have a team of award-winning customer service agents based in Cardiff. They’re online 24/7 every day, including Christmas Day. ANNA Money is the business current account for start-ups, small businesses and sole traders. You even get free Bookkeeping software for UK small businesses and sole traders with it. Account set up takes less than 10 minutes, and your business debit card will be on the way the same way. Try ANNA for free, starting today. Simply follow the link below. It’s safe and secure.

Save time and save money. Sign up now. FCA Regulated and your money is protected. See video to see how you are protected.  I am struck by how many of the business owners I meet that do not consider this, and when I raise the subject, they usually tell me that they are relying on a private rental property and a modest pension for their retirement with no further access to finance.

They do not see their business as a saleable asset but as a source of cashflow that will have no value when they stop working And so often when I look at the financial structure of their business, its only assets are the debtor book, (some of which isn’t collectible), creditors at about the same value as the debtors, some cash in the bank and equipment and stock which would fetch less than book value if sold off. It’s therefore true, such a business is really not saleable, just something to close down and walk away from; as do 250,000 other UK small businesses owners every year for this very same reason. However, majority could be sold for a six or seven figure sum if managed differently Such an amount would transform the owners’ retirement finances from ‘getting by’ to luxury. Yet I get strong objections to the above proposition such as, “this business is all about me, so it isn’t saleable” I politely disagree with the above and put it to you that any and every business is saleable How? Well, it is instructive to first look at big businesses, which are all about money and return of investment (ROI) to see what they do. The aim is to not to be as ruthless as them but to learn for free what you can adapt. Here is what they do (just in their financial management stream – there are 4 others*):

At face value, much or all of this sounds time-consuming, costly and bureaucratic. To an extent it is. However, big businesses perform the above actions for the very good reason that it works, knowing that time invested in doing this provides a very good payback and ensures their survival. And remember, every big business was once a little one whose founders had the foresight to introduce strong business performance strategies and financial management at an early stage. The average big business sells for 14x pre-tax profits. Yet I have seen small businesses making £50K pa close down for instead of selling as a going concern for £500K+ It may seem that chasing another order or dealing with a customer crisis is a better use of your time. However, it should account for all you do. Appropriate business and financial management would make the orders come in automatically and prevent the customer problem in the first place. Knowledge is power and good financial management and other applicable actions gives you the power to make smart decisions that will build a saleable business worth millions. Most of what I have instanced above are not difficult to implement. And if you find this a challenge, your Business Advisor at RBSS Consulting Ltd, Romford will do it for you, helped by low-cost apps. Please note: not every action mentioned above will apply to your business which is a good reason to call in an experienced and professional Business Advisor for expert guidance. If you can resonate with some of the above points or are in any doubt as to which direction your business is heading in, get in touch with us today and you can be rest assured we will point and lead you in the right direction at RBSS Consulting Ltd. _______________________________________________________________ Your first step is for free and takes 15 minutes by Booking a free assessment here to find out how much your business is worth today, what it should be worth, and the actions needed to get it there. All in a comprehensive report tailored just for you. Another RBSS Consulting Business Consultant service… “Delivering Real Business Solutions” (*The 5 business streams are Marketing; Operations; Systems; People; Finance)  Every business whether start-up or existing micro, small, medium or large enterprise, needs expert and valuable business advice. That’s where RBSS steps in. We provide a full diagnostic on areas of your business or field you may not have thought about, but are important. A business consultant can also be an excellent sounding board to help get you out of some very tricky situations. Some business solutions are ways to raising finance, business valuation and health checks, business planning , growth strategies, profitability and efficiency strategies, business modelling etc. These services are available to both start-ups and existing businesses.

In this blog I will focus on 4 key areas a consultant can add value to your business.  All credit to Rita Gunther McGrath on this blog. She’s the author of – The end of competitive advantage. She says that: ‘organisations need to forge a new path to winning: capturing opportunities fast, exploiting them decisively, and moving on even before they are exhausted. With this book she explains a new set of practices based on the notion of transient competitive advantage. She shows how some of the world’s most successful companies use this method to compete and win today.’

There are many reasons for business failure. From poor management and not following the business plan, to bad market research, to poor marketing strategies - the list goes on. From the outside, it can be easy to spot what someone isn’t doing right, but when you’re on the inside it’s not so easy to see the mistakes being made, even when you’re the one making them. Below we look at three common business mistake to avoid that could save your business from going under.

|